Introductions

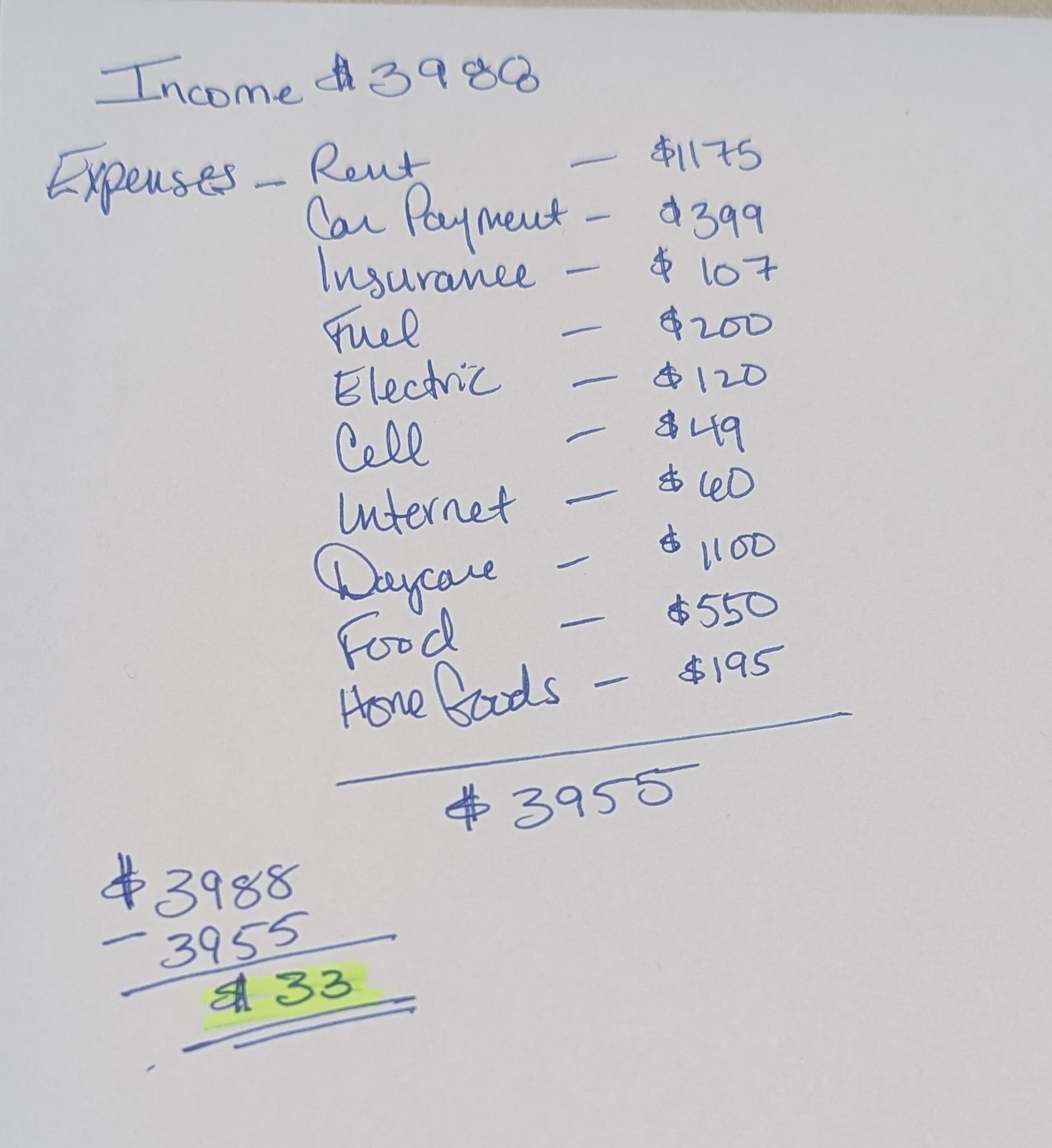

Meet Monica, a single mother of two who earns $70,000 a year. After taxes, $478 a month in health insurance premiums, and union dues, her take-home pay is $3,488 a month. She also receives $500 a month in child support, bringing her total monthly income to $3,988. Here is where it goes:

Rent: $1,175

Car payment: $399

Car insurance: $107

Fuel: $200

Electric: $120

Cell phone: $49

Internet: $60

Daycare for both kids: $1,100

Groceries: $550

Household and personal care: $195

Monica found an affordable, quality licensed care center that runs $550 per child per month and keeps both kids from 8:30 to 5:30. Without it, she cannot work. She's grateful that it's an excellent center with teachers the kids love, but wonders if she should consider a cheaper alternative despite its quality.

Her grocery budget is $550 a month. That covers real food for her family of three, two of whom are toddlers who go through Cheerios, applesauce, and Goldfish crackers at a pace that does not care what the checking account looks like. She shops Great Value when she can and watches the sales. She makes taco night stretch and shreds the chicken off the bone because no parent is handing a toddler a chicken thigh, even if they are cheaper.

If you add it up, you'll find that Monica has $33 left each month.

Thirty-three dollars when she doesn't include a birthday gift for the kid in Sarah's class who handed out invitations at daycare. Or make space for a trip to the doctor when Luke wakes up with a fever at 2am. It doesn't include a Happy Meal on a Friday night when Monica has worked five days, loaded and unloaded two toddlers from their car seats, cooked dinner every single one of those days, done bath time and argued about brushing teeth and read the story for a third time as demanded. It doesn't even leave room for an oil change.

An oil change at Walmart runs $60 to $80, and she cannot skip it. The car is how she gets to work, how she gets the kids to daycare, how the whole fragile structure stays standing.

Monica pays for health insurance for herself and the kids. She found affordable, quality childcare. She earns $70,000 a year, which puts her comfortably above what we learned last month is the local median posted wage of $15.25 an hour.

Despite this, she can not afford to buy a home. To qualify for a median three-bedroom house in Pickens County under standard lending guidelines, a household needs to earn around $95,120 a year. That leaves a $25,000 income gap that isn't a budgeting problem. There is no combination of coupons and sacrifice that closes it. It is simply the cost of admission to homeownership in this county, and Monica can't meet it.

She's not alone in this.

Josh and his wife Rebecca both work. Together they bring home just over $63,000 a year, both of them earning wages typical of what local job postings show. They have two boys, Jake and Landon.

Like most young families, they faced the kind of decision that has no good answer. Rebecca could stay home with the boys while they were young, but that would mean surviving on one income. Josh didn't earn enough to cover rent on his own. So she went back to work, which meant paying someone else to watch the kids.

They chose two incomes and for years, full-time daycare for both boys consumed a significant portion of what Rebecca brought home. Now Jake and Landon are both in school and they are finally catching their breath. After school care still runs $250 per boy per month, but the School District of Pickens County provides free breakfast and lunch, which helps a lot. Jake started Little League, which comes with registration fees and cleats that fit this season but probably not next, but they're doing okay

Despite this their income is still $31,000 short of what they need to qualify for a median home purchase in Pickens County.

They are not struggling in ways that are easy to see. They go to work. The kids are fed. The bills get paid. But the door to the next chapter of their lives will not open, and every year it stays closed is a year their boys spend in a rental, in a neighborhood that is not quite theirs, in a school they may or may not still attend next fall.

That last part matters far more than most discussions about housing affordability acknowledge.

The Research

Habitat for Humanity International's research series on homeownership outcomes documents what stable housing actually produces in a family's life. Residential stability is linked to improved educational outcomes for children, better physical and mental health, stronger civic participation, and greater life satisfaction (via habitat.org). For lower and moderate income households specifically, a $10,000 increase in housing wealth raises the probability of a child attending college by 14 percent (via habitat.org). The CDC has identified housing as a social determinant of health.

When researchers study homeownership, they consistently find improvements in educational outcomes, health outcomes, civic engagement, and financial stability. The reason may be simpler than it sounds. Homeownership allows families to stay put. The benefits researchers measure may be the benefits of stability itself.

These are not arguments for why homeownership is a nice thing to have. They are documentation of what instability costs. Every year Jake and Landon spend moving is a year of interrupted friendships, new classrooms, teachers who do not yet know their names. The research is not subtle about what that accumulates into.

Among recent Pickens County Habitat for Humanity applicants, 36 percent reported moving every year. Those are people who live and work right here in our county. They are our neighbors.

Sometimes they move because the rent went up. Sometimes they move because the unit that looked affordable turned out to have roaches in the kitchen or black mold growing in the closet of the kids' bedroom, the result of a bathroom leak that was never repaired.

Research from Habitat for Humanity International found that removing asthma triggers like mold and pests from homes led to decreased healthcare use and improved quality of life for children (via habitat.org). The house itself can be making the family sick. And when you can't afford to be selective, you move and hope the next place is better.

Every move might require a payment of first month's rent, last month's rent, and a security deposit. At the median advertised rent of $1,200 a month in Pickens County, that often means $3,600 before a single box is moved. Families who relocate repeatedly are not failing to save for homeownership. They are repeatedly spending what they save just to remain housed.

And every move costs more than money. It costs the pediatrician who knew your child's history. It costs the neighbor who watched your kids when you had a late shift. It costs the slow accumulation of community that research consistently finds is one of homeownership's most durable benefits. You can't build roots while you are moving every twelve months. You can't build equity. You can't build the kind of stability that the data shows changes outcomes for children, for health, for everything that comes after.

Health is where the math gets most complicated.

Eric brings home roughly $4,000 a month. By every standard measure, he looks like someone who has it figured out. He is also chronically ill.

When a better job opened up in another city, Eric took it. He covered first month, last month, a security deposit, and a moving truck. He found a place he could afford and he settled in. Then he did the slow, unglamorous work of rebuilding his medical life from scratch. New primary care physician. New specialist, with the months-long wait that comes with finding one taking new patients. New pharmacy. New providers reading his chart cold and asking questions his old doctors stopped asking years ago.

He waited six months for his rheumatology referral to result in an appointment. A year for neurology. But he got there.

Most people understand what it means to finally find a doctor they trust. For someone managing multiple chronic conditions, losing a specialist is not an inconvenience. It can mean losing access to the treatment that makes working, and everything else, possible.

The house helped too. A three-bedroom rental with a backyard. Enough space for family to visit and still leave him room for a home office. On the days when his illness made the commute impossible, he could work from home. It was not perfect. But it was stable, and for someone managing a chronic illness, stability is not a luxury. It is part of the treatment plan.

Then he got the news: his landlord was selling the house. The only replacement Eric could find that fit his budget is not close to his job and not close to his doctors. He now drives 45 minutes to work and an hour each way to see the physicians he spent years getting in with. He kept the doctors because starting over a second time was not something his health could survive.

And then there is the cost. From the outside, Eric's finances look stable. A good salary, a budget he manages carefully, nothing obviously wrong. But the health of a system, or a person, can be very deceiving. Every month Eric pays his insurance premium to keep his care team intact. Then his prescriptions, some of which his insurance classifies as tier three, the expensive tier. Then his copays, $50 for primary care and $100 for each specialist visit. A recent MRI cost him $700 out of pocket. A single lab panel was priced at $5,000. His insurance covered all but $300, which felt like a relief until he remembered that $300 does not exist in a vacuum. It sits on top of everything else.

None of these costs are catastrophic in any single month. Unless something shows up in a lab. A single concerning value can set off a cascade, a repeat test, a referral, a specialist copay, imaging, follow-up appointments, and suddenly a month that was manageable is not. And if that cascade results in ongoing monitoring, which it sometimes does, Eric now carries a new recurring expense that was not in last month's budget and will be in every budget going forward.

He can't move closer to his doctors because he can't afford to. He can't start over with a new care team because for someone managing multiple chronic conditions, a year without a specialist is not a scheduling problem. It is a health crisis. Without regular neurological care alone, Eric risks losing his ability to work entirely. The conditions he manages don't pause while he waits for a new provider to have an opening. They progress. And some of that progression can't be undone.

Every option that would make his life more manageable requires the one thing he doesn't have - a home he can't be forced out of.

Behind the Curtain

Monica's challenge is childcare and wages. Josh and Rebecca's challenge is that two incomes still are not enough. Eric's challenge is that the system can't see what his health actually costs him. The details are different. They arrive at the same place.

Pickens County Habitat for Humanity exists because the market, on its own, does not reach Monica. It does not reach Josh and Rebecca. It does not reach Eric. It does not reach the 36 percent who moved last year and will move again this year unless something changes.

We are not in the business of charity. We are in the business of closing the gap between where families are and where the door is. And we are deliberate about how we do it. The neighbors who build and buy Pickens County Habitat for Humanity homes are partners in that process from the beginning. They put in the hours. They learn the systems. They carry the responsibility. We work alongside them to make sure that when they cross that threshold, they are ready for what comes next, that the mortgage fits, that the support is there, and that homeownership delivers what the research promises it can.

What they cannot do alone is manufacture an entry point that the market has priced out of reach. If you are ready to help close that gap, we would be grateful to have you with us.